Article

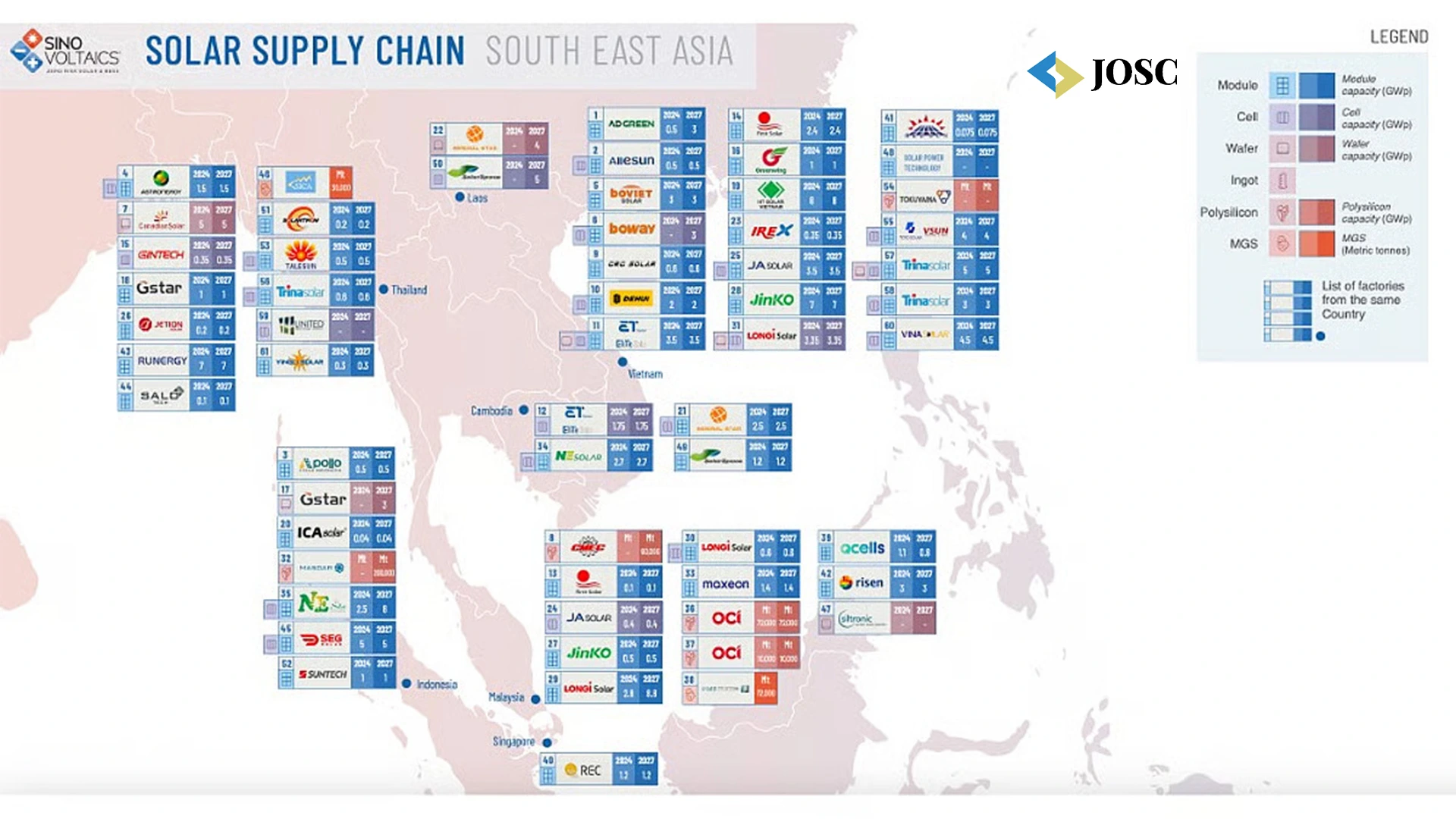

Southeast Asia Solar Supply Chain Map 2025

Anamika Mishra,

Sub Editor

Anamika Mishra,

Sub Editor

Hong Kong-based Sinovoltaics has recently released the inaugural edition of its Southeast Asia Solar Supply Chain Map 2025, offering valuable insights into the rapidly changing solar manufacturing landscape in the region. This report forms part of Sinovoltaics’ global market intelligence series, which provides comprehensive regional maps that detail the key manufacturers and suppliers spanning the entire solar value chain from polysilicon and wafers to solar cells and modules.

Key Trends and Disruptions in Southeast Asia

Once considered viable alternatives to China for solar manufacturing, Southeast Asian countries like Vietnam, Thailand, and Cambodia are now facing significant disruptions. This shift is primarily due to U.S. import tariffs, which have hit the operational capacities of these nations hard. As a result, there is a visible reorientation of manufacturing activity toward countries like Laos and Indonesia, which currently lie outside the scope of the tariffs.

Manufacturers are adapting by diversifying export markets, particularly toward Europe and emerging hubs in the Middle East, as they navigate trade tensions and seek tariff-free access to global markets.

New Players and Regional Growth

The report also highlights the entry of new manufacturers, such as ICA Solar and United Renewable Energy (URE), both of which have recently expanded operations in the region.

Southeast Asia is experiencing one of the fastest growth rates in solar manufacturing worldwide. The region’s nameplate photovoltaic (PV) module capacity stands at 86 GW and is forecast to grow to 101 GW by 2028–2030. Similarly, cell manufacturing capacity, currently at 51.3 GW, is expected to rise to 69.8 GW by 2030.

The upstream sector is also booming. Ingot production is set to nearly double from 16 GW to 30 GW, backed by a dramatic increase in polysilicon production, from 82,000 metric tonnes to 342,000 metric tonnes. Additionally, Southeast Asia is projected to add 102,000 metric tonnes of metallurgical-grade silicon (MG-Si) capacity to support this upstream expansion.

Comparison with India’s Solar Manufacturing Landscape

India, another major player in the global solar supply chain, has been aggressively promoting domestic solar manufacturing through initiatives such as the Production Linked Incentive (PLI) Scheme, the “Make in India” campaign, and customs duties on imported solar cells and modules.

While India's manufacturing capacity is growing steadily, the Southeast Asian surge poses both challenges and opportunities:

1. Competition for Investment and Market Share

Southeast Asia’s rapid shift and expansion in solar manufacturing capacity, especially in countries like Indonesia and Laos, could attract a significant portion of foreign direct investment (FDI) that might otherwise have flowed into India. These emerging hubs are becoming increasingly appealing to global investors due to their strategic advantages and growing industrial ecosystems. This trend poses a challenge for India as it vies to establish itself as a dominant player in the global solar supply chain.

However, the imposition of U.S. tariffs on several Southeast Asian countries limits their access to one of the world’s largest solar markets. This situation presents a valuable opportunity for India to carve out a competitive advantage in exports to the United States. By ensuring compliance with stringent quality standards and traceability requirements, Indian manufacturers can position themselves as reliable suppliers to the U.S. market. Capitalizing on this opportunity will require India to strengthen its manufacturing capabilities, enhance transparency in its supply chains, and align with international regulatory frameworks, thereby turning global trade challenges into a strategic advantage.

2. Supply Chain Dependencies

India continues to rely heavily on imports for critical raw materials required in solar manufacturing, particularly polysilicon and wafers most of which are currently sourced from China. This dependence poses a strategic vulnerability, especially in the context of fluctuating trade relations and global supply chain uncertainties. For a country aiming to build self-reliance in the renewable energy sector under the Aatmanirbhar Bharat initiative, reducing this overdependence is essential.

In this context, the rapid expansion of upstream manufacturing capabilities in Southeast Asia presents a timely opportunity for India. Countries such as Indonesia, Malaysia, and Vietnam are ramping up their production of key materials like polysilicon and metallurgical-grade silicon (MG-Si), creating a more diversified and accessible supply base within the region. These emerging suppliers could serve as viable alternatives to China, helping India de-risk its solar value chain while maintaining competitive sourcing options.

By actively engaging with Southeast Asian manufacturers through long-term contracts, strategic partnerships, or joint ventures, India can secure a stable and politically neutral supply of raw materials. This would not only strengthen the resilience of India’s domestic solar manufacturing industry but also support the broader goal of becoming a global hub for clean energy technologies.

Ultimately, tapping into Southeast Asia’s growing upstream ecosystem aligns perfectly with India’s vision of reducing import dependence and creating a more secure, self-sustaining solar supply chain.

Conference

Conference

Conference

Summit

Conference

Conference

Conference

3. Opportunity for Collaboration

The recent boom in Southeast Asia’s solar supply chain presents a unique opportunity for India to engage in meaningful cross-border collaboration, especially at a time when the global focus is firmly on clean energy and sustainable growth. As countries like Indonesia, Vietnam, and Laos expand their solar manufacturing capacities, a new regional ecosystem is taking shape, one that is ripe for partnerships in areas such as joint ventures, technology transfers, and integrated supply chains. For India, which is also on a strong growth trajectory in renewable energy, this is an opportune moment to position itself not just as a competitor, but as a strategic collaborator in building a green energy bloc across Asia.

India’s solar manufacturing ambitions can greatly benefit from technological cooperation with Southeast Asian nations that are investing heavily in upstream and midstream production such as polysilicon, ingots, and wafers. By entering into joint ventures or technical licensing agreements, Indian companies can gain access to advanced technologies, reduce their reliance on China, and improve the cost-efficiency and quality of domestic manufacturing. At the same time, Indian firms can bring value to the table with their engineering talent, large domestic market, and growing policy support for renewables.

Moreover, as Southeast Asian countries face U.S. tariffs and shift their focus towards European and Middle Eastern markets, India can collaborate with them to form export-oriented consortia. These consortia could optimise production across borders, reduce redundancy, and create shared value chains that benefit all participating nations. With proper government-to-government engagement and support from regional trade bodies, such collaborations could help create a more self-reliant and politically balanced solar supply network in the Indo-Pacific region.

India can also take the lead in pushing for regional policy dialogues and joint R&D initiatives focused on innovation in solar efficiency, battery storage, and grid integration. Establishing a South and Southeast Asian Clean Energy Forum could help synchronize efforts, align standards, and accelerate the deployment of clean technologies across the region.

In essence, the growth of Southeast Asia’s solar manufacturing sector should not be seen merely as competition, but as a gateway to building regional energy resilience. For India, this is a chance to reinforce its leadership role in the clean energy transition while fostering long-term economic and technological partnerships that go beyond borders.

4. Strategic Policy Alignment Needed

To secure its position in the fast-evolving global solar manufacturing landscape, India must act with urgency and purpose. One of the most pressing needs is the rapid development of industrial infrastructure. This includes setting up dedicated solar manufacturing zones, improving transport connectivity, and ensuring uninterrupted access to essential utilities like electricity and water. Without robust infrastructure, India risks falling behind countries in Southeast Asia that are already moving swiftly to attract large-scale investments in solar manufacturing.

Equally important is the streamlining of land acquisition and utility access, which continue to be major bottlenecks for solar manufacturers in India. Lengthy approval processes, unclear land titles, and regulatory red tape often delay projects and increase costs. There is a clear need to simplify procedures, introduce single-window clearances, and offer plug-and-play industrial land with ready access to power, water, and logistics services. This would go a long way in making India a more attractive and efficient destination for solar investments.

Another critical area is investment in research and development (R&D). As solar technology continues to evolve globally with innovations such as high-efficiency cells, bifacial modules, and new materials, it is essential for India to build a strong base in R&D. This can be achieved through increased government funding, closer collaboration between academia and industry, and incentivising innovation through tax benefits and grants. A strong R&D ecosystem will not only boost quality and productivity but also help Indian manufacturers compete on a global stage through technological leadership.

In addition to physical and intellectual infrastructure, targeted policy reforms will be the key to unlocking India’s true potential in solar manufacturing. The government’s initiatives like the Production Linked Incentive (PLI) scheme are steps in the right direction, but they must be implemented more effectively and expanded to cover the entire solar value chain from polysilicon to modules. Timely disbursement of incentives, rationalisation of import duties on critical equipment, and dedicated support for upstream segments are all essential to match the pace of Southeast Asia, where countries like Indonesia and Vietnam are making rapid strides.

India must also remain agile in responding to global developments such as changing trade policies, shifting supply chains, and evolving environmental standards. A focused policy think-tank for the solar sector could help India stay ahead of these changes. With coordinated efforts across infrastructure, policy, and innovation, India can not only match but potentially outpace Southeast Asia in becoming a global solar manufacturing powerhouse.

A Regional Realignment with Global Impact

The 2025 Sinovoltaics report brings to light the rapid evolution taking place in Southeast Asia’s solar supply chain. With U.S. import tariffs disrupting established manufacturing bases in countries like Vietnam, Thailand, and Cambodia, a noticeable shift is now underway toward emerging players such as Laos and Indonesia. These newer markets, currently outside the scope of U.S. trade restrictions, are fast becoming attractive destinations for solar manufacturing investments and exports. While these developments are rooted in Southeast Asia, their implications stretch far beyond the region and India must take note.

For India, this shift presents both a challenge and a valuable opportunity. On the one hand, the aggressive capacity expansion in Southeast Asia, especially in upstream segments like polysilicon and ingots, increases competition. Countries like Indonesia are positioning themselves as serious contenders, drawing global interest and investment. This could, if not addressed strategically, threaten India's efforts to become a leading global hub for solar manufacturing.

However, there is a clear silver lining. As U.S. tariffs steer export flows away from Southeast Asia, India is uniquely positioned to step into the gap particularly if we continue to improve our manufacturing competitiveness and meet international standards around quality, traceability, and sustainability. With our own Production Linked Incentive (PLI) schemes and strong policy support for renewable energy, India already has a foundation in place. What’s needed now is a faster and more focused execution of infrastructure, supply chain development, and skilled manpower.

Moreover, the evolving Southeast Asian supply chain could also complement India’s ambitions. With increased production of polysilicon and MG-Si in the region, India has the chance to reduce its long-standing dependence on Chinese imports by sourcing materials from friendlier markets. This diversification would strengthen our self-reliance in solar manufacturing and align with the broader goals of Aatmanirbhar Bharat.

India must also explore strategic partnerships across Asia. Whether through joint ventures, technology collaborations, or cross-border supply chain integration, working together with countries in Southeast Asia could create a powerful, regional green energy ecosystem.

In summary, while the Southeast Asia supply chain realignment brings increased competition, it also opens a door for India to assert itself as a global solar leader. With timely policy action, smart investments, and regional cooperation, India can not only withstand the shifting dynamics but emerge stronger, driving both national and global progress toward clean energy goals.

Explore the latest edition of Journal of Supply Chain Magazine and be part of the JOSC News Bulletin.

Discover all our upcoming events and secure your tickets today.

Journal of Supply Chain is a Hansi Bakis Media brand.

Leave Comment

Join the community of 150,000+ industry professionals

Subscribe to our Daily Newsletter

Subscribe For FreeBy continuing you agree to our Privacy Policy & Terms & Conditions

Latest

Feature Articles

Related